{kind=link}

Filing a roofing insurance claim in Colorado is one of the most stressful experiences a homeowner can face — especially when the damage came from an event you couldn’t control, like a hailstorm, high wind event, or fallen tree limb. You’re already dealing with property damage, and now you have to navigate insurance company processes, adjuster meetings, contractor estimates, and paperwork.

The good news: while the process can feel overwhelming, it’s actually fairly predictable once you understand the steps. Knowing what to do — and what to avoid — can mean the difference between a full, fairly-paid claim and a frustrating denial or underpayment.

This guide walks you through every step of filing a roofing insurance claim in Colorado, from the moment damage occurs through the final depreciation check. Whether you’re dealing with hail damage, wind damage, or storm damage from any cause, the process and your rights as a Colorado homeowner are largely the same.

Step 1: Don’t Call Your Insurance Company First

This is the most counterintuitive piece of advice in the entire process, but it’s also the most important. The natural impulse after damage is to immediately call your insurance company. Resist that impulse.

Here’s why: insurance adjusters often inspect roofs without a contractor present, and their inspections frequently miss damage that a roofing professional would catch. When the adjuster’s report becomes the basis of your claim, missed damage means missed coverage. Once a claim is opened and an initial scope of loss is written, it becomes harder to add items later.

Instead, your first call should be to a licensed local Colorado roofing contractor for a free, no-obligation inspection. Reputable roofers in Colorado Springs and across the Front Range will perform this inspection at no cost and provide detailed photographic documentation of any damage they find.

This documentation becomes your foundation for the entire claim. With professional damage records in hand, you’ll be in a far stronger position when you contact your insurance company.

Step 2: Get a Professional Roof Inspection

Schedule your free inspection within a few days of the damage event. The longer you wait, the harder it becomes to prove the damage came from a specific storm rather than gradual wear.

A thorough professional inspection should include:

- A complete walkable inspection of the roof surface (or drone inspection for very steep roofs)

- Photographic documentation of every area of damage — close-ups and wide shots

- Measurements of damaged sections

- A detailed written report describing the nature, extent, and likely cause of damage

- An itemized estimate for repair or replacement work

- Notes on related damage to gutters, downspouts, fascia, soffits, siding, and any interior leak signs

If a “roofer” wants to skip any of these steps or refuses to provide written documentation, find a different contractor. Reputable companies provide this documentation as a standard part of their free inspection.

Keep the inspection report in a safe place — you’ll reference it multiple times throughout the claim process.

Step 3: Review Your Insurance Policy Before Filing

Before opening a claim, pull out your homeowner insurance policy (or log in to your insurance company’s online portal) and review the relevant sections. You’re looking for:

Your deductible amount. This is what you’ll pay out of pocket before insurance coverage kicks in. Standard deductibles range from $500 to $2,500 for most policies, though some Colorado policies use a percentage-based deductible for wind/hail damage (often 1-5% of the dwelling coverage amount).

Whether your coverage is ACV or RCV. This is critical:

- ACV (Actual Cash Value) policies pay the depreciated value of your roof. A 15-year-old roof would only be covered for a fraction of replacement cost.

- RCV (Replacement Cost Value) policies pay the full cost to replace your roof with new materials of similar kind and quality, regardless of age.

If you’re not sure which you have, call your agent and ask. The difference can be thousands of dollars on a single claim.

Your wind/hail coverage limits and exclusions. Some policies have specific exclusions for cosmetic damage, restoration limits, or named-peril restrictions. Read this section carefully.

The claim filing deadline. Most Colorado policies have a 1-year window from the date of loss to file a claim, but some require notice within 60 or 90 days. Don’t assume you have a year.

Step 4: File Your Claim

With your professional inspection report in hand and policy reviewed, you’re ready to contact your insurance company. Call the claims phone number on your policy or file online through your insurance company’s portal.

When you file, you’ll need to provide:

- The date of loss (when the damage occurred — typically the date of the storm)

- A brief description of the damage

- Your contact information

- Your contractor’s information (their company name and contact details — many insurance companies will want to coordinate with them)

The insurance company will assign you a claim number and either schedule an adjuster visit or ask you to provide additional information first. Get the adjuster’s name, phone number, and email — you’ll need to coordinate with them in the next step.

Step 5: Schedule the Adjuster Meeting With Your Contractor Present

This step is non-negotiable: when the adjuster comes to inspect your roof, your contractor MUST be there too.

This is where most homeowners lose money on their claims. When the adjuster visits alone, they may:

- Miss damage that requires a trained roofer’s eye to spot (especially hail bruising on shingles)

- Underestimate the scope of work needed

- Use outdated unit pricing for materials and labor

- Omit code-required upgrades (proper underlayment, ice and water shield, drip edge, ventilation)

- Skip related damage to gutters, soffits, or flashing

When your contractor is present, they walk the roof alongside the adjuster, point out specific damage areas, discuss building code requirements, and negotiate the scope of work in real time. The result is almost always a more complete and accurate claim approval.

To set this up: once the adjuster gives you a window for their visit (often a 2-3 hour window), call your contractor and have them confirm they’ll be at your property during that time. The adjuster meeting itself typically takes 1-2 hours.

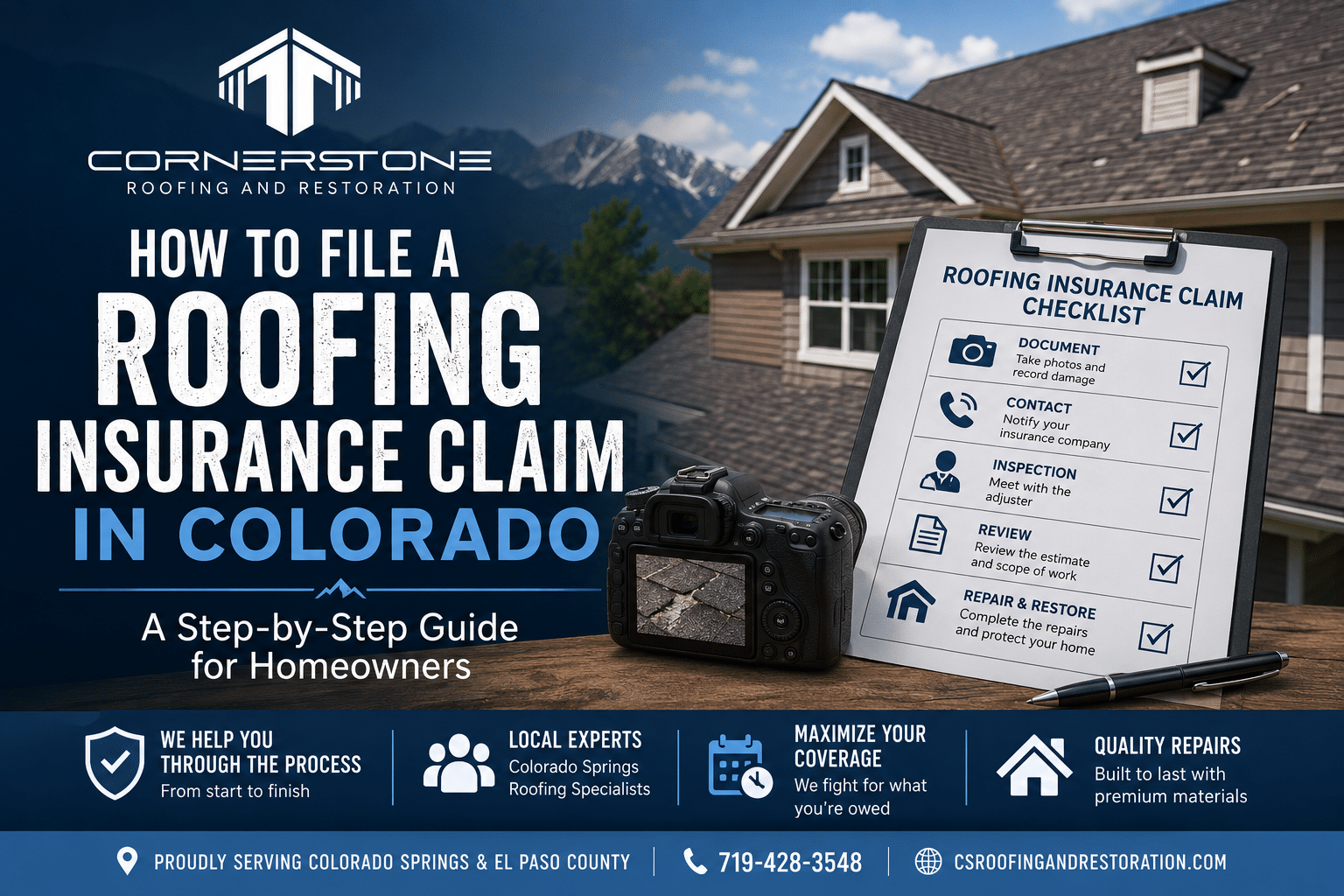

Step 6: Review the Scope of Loss Document

After the adjuster’s inspection, the insurance company will send you a “Scope of Loss” document — sometimes also called an Estimate, Adjustment, or simply “the paperwork.” This is the insurance company’s itemized list of what they’re agreeing to pay for.

Your contractor should review this document with you line by line. Common issues to look for:

- Missing line items. Did the adjuster include all the materials needed (ice and water shield, synthetic underlayment, drip edge, ridge vent, etc.)?

- Inadequate quantities. Are the measurements accurate? Did they include proper waste factor?

- Outdated pricing. Material and labor costs in Colorado have risen significantly in recent years. Old unit prices can leave you thousands short.

- Missing code upgrades. Colorado building codes may require improvements (ice barrier, enhanced ventilation, etc.) when more than a certain percentage of roofing is replaced.

- Omitted related damage. Damaged gutters, soffit, fascia, flashing, and skylights are commonly missed.

If you find issues, you don’t argue with the adjuster directly. Instead, your contractor files a “supplement.”

Step 7: Work Through Supplements

A supplement is a formal request to the insurance company to add or correct items in the scope of loss. Most roofing claims involve at least one supplement — sometimes two or three.

To file a supplement, your contractor sends the insurance company:

- A written explanation of what was missed or underpaid

- Photographic evidence supporting the request

- An updated estimate with corrected line items

- Reference to relevant building codes or manufacturer specifications

Insurance companies process supplements within 7-30 days, depending on their internal workflow. Reputable contractors handle this entire process on your behalf — you shouldn’t have to write supplement letters or argue with adjusters yourself.

Don’t be alarmed if your claim requires multiple supplements. This is normal. The system is designed for back-and-forth refinement, and a contractor who knows the process can typically secure thousands of dollars in additional coverage through supplements.

Step 8: Receive Your First Insurance Check (ACV Payment)

Once the scope of loss is finalized and any supplements are approved, your insurance company will issue the first check. This is typically the ACV (Actual Cash Value) amount, which equals:

Total claim amount − Your deductible − Depreciation (held back for the second check) = ACV Check Amount

For example, if your total approved claim is $15,000 with a $1,000 deductible and $3,000 in depreciation withhold, your first check would be $11,000.

Two important notes about this check:

- Your mortgage company may need to endorse it. If you have a mortgage, your mortgage company is typically named as a co-payee on insurance checks over a certain threshold (often $20,000+). You’ll need to mail the check to your mortgage company for endorsement before depositing.

- You pay your contractor with this money, not extra. This is the insurance company’s payment for the work. Apply it directly toward your contractor’s invoice.

Step 9: Roof Replacement Begins

With the first check in hand and final scope approved, your contractor schedules the actual installation. Most Colorado Springs residential roof replacements take 1-3 days of on-site work, plus additional time for material delivery and final inspections.

During the project:

- Protect interior valuables near skylights or above ceiling areas being worked on

- Keep children, pets, and vehicles clear of the work area

- Expect noise from morning to mid-afternoon (typically 7 AM – 4 PM)

- Ask your contractor about their daily cleanup process

A reputable contractor will perform multiple magnetic sweeps of your driveway and lawn before leaving each day, especially the final day. Stray roofing nails can damage tires and injure pets, so cleanup is critical.

Step 10: Final Documentation and Depreciation Release

Once the work is complete, your contractor sends final documentation to your insurance company:

- A final invoice marked “Paid in Full”

- A Certificate of Completion

- Photos of the finished work

- Any updated permits or inspection certificates

The insurance company then releases the depreciation portion of your claim — the difference between your initial ACV payment and the total Replacement Cost Value. Using our earlier example, this would be the additional $3,000.

If your contractor performed any approved supplements during the project, those are also reconciled at this stage. Total time from job completion to final depreciation check is typically 14-30 days.

Common Pitfalls to Avoid

Don’t sign anything that releases your right to insurance proceeds. Some contractors use AOB (Assignment of Benefits) forms that transfer your claim rights to them. In Colorado, this is generally legal but rarely in the homeowner’s best interest. Decline AOB requests.

Don’t accept “deductible-free” offers. Any contractor who offers to absorb or waive your deductible is violating Colorado law and pulling you into insurance fraud. This is grounds for both criminal charges and claim denial.

Don’t let your claim go unfiled past the deadline. Most policies require notice within 1 year, but file as early as possible. Late claims face additional scrutiny.

Don’t work with out-of-state storm chasers. Door-knocking crews that appear after major storms often lack local licensing, file improper claims, and disappear when warranty issues arise. Always verify Colorado licensing and local references.

Don’t agree to a roof scope based on the adjuster’s first estimate alone. Have your contractor review every line item before you sign anything.

Frequently Asked Questions

Will filing a roofing insurance claim raise my premium?

For most Colorado homeowners, the answer is no — at least not directly. Hail and storm damage claims are considered “act of nature” claims, which insurance companies generally don’t penalize through premium increases the way they do for liability claims. However, multiple claims over a short period can affect renewal terms. If you’re considering filing, discuss specifics with your agent.

What if my insurance company denies my roofing claim?

First, request the denial in writing with specific reasons. Have your contractor file a formal supplement addressing each denial reason with additional documentation. If the denial stands, you can request a re-inspection with a different adjuster, file a complaint with the Colorado Division of Insurance, or hire a public adjuster to advocate on your behalf.

Do I have to use the contractor my insurance company recommends?

No. You have the right to choose your own roofing contractor in Colorado. Insurance companies often have “preferred contractor” networks, but you’re never obligated to use them. In fact, a contractor who works for you (not the insurance company) is more likely to advocate for full coverage on your behalf.

How long do I have to file a roofing insurance claim in Colorado?

Most homeowner policies in Colorado allow up to 1 year from the date of loss, though some have shorter notice windows. Check your specific policy. Acting within 30-60 days of the damage gives you the best chance of clean claim approval.

What does my deductible apply to?

Your deductible applies once per claim, not once per item damaged. If your roof, gutters, siding, and skylight were all damaged by one storm, you pay your deductible once and the insurance covers the rest (subject to your coverage limits).

Get Expert Help With Your Colorado Insurance Claim

Filing a roofing insurance claim alone is possible, but having an experienced contractor as your advocate dramatically improves the outcome. At Cornerstone Roofing & Restoration, we’ve guided hundreds of Colorado homeowners through successful insurance claims. We handle the documentation, attend adjuster meetings, file supplements, and fight for the full coverage you’re entitled to.

We’re licensed in Colorado, fully insured, and IKO-certified. Most importantly, we work for you — not the insurance company.

Call (719) 600-7852 today for a free, no-obligation roof inspection and claim consultation.

We proudly serve Colorado Springs, Monument, Castle Rock, Aurora, Black Forest, Peyton, Manitou Springs, Gleneagle, Larkspur, Stratmoor, and all surrounding Front Range communities.